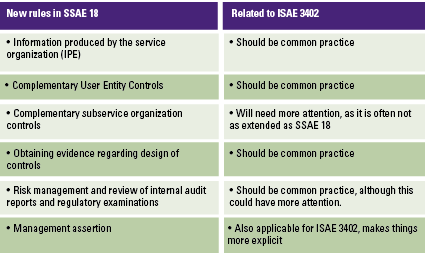

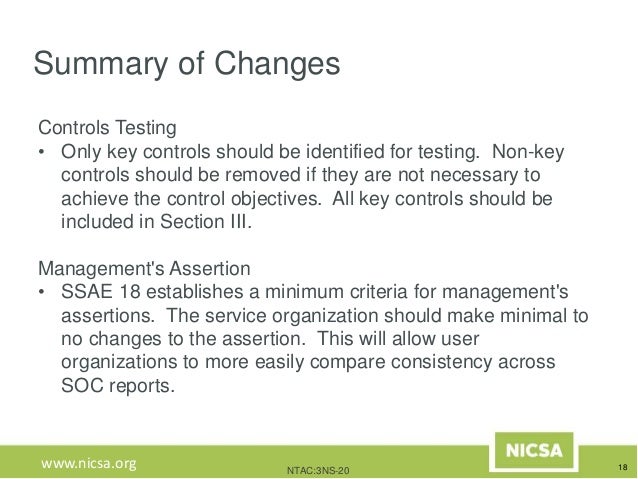

Ssae 18 Control Objectives List

The Astounding Ssae 16 Audit Soc 1 Soc 2 Soc 3 From Lazarus Alliance With Regard To Ssae 16 Report In 2020 Best Templates Professional Templates Business Template

The New Us Assurance Standard Ssae 18 Compact

The Clarity Project Ssae 18 Essentials

Https Guidehouse Com Media Www Pdfs Legacy Guidehouse Whitepapers What Are Ssae No 18s And How Pdf

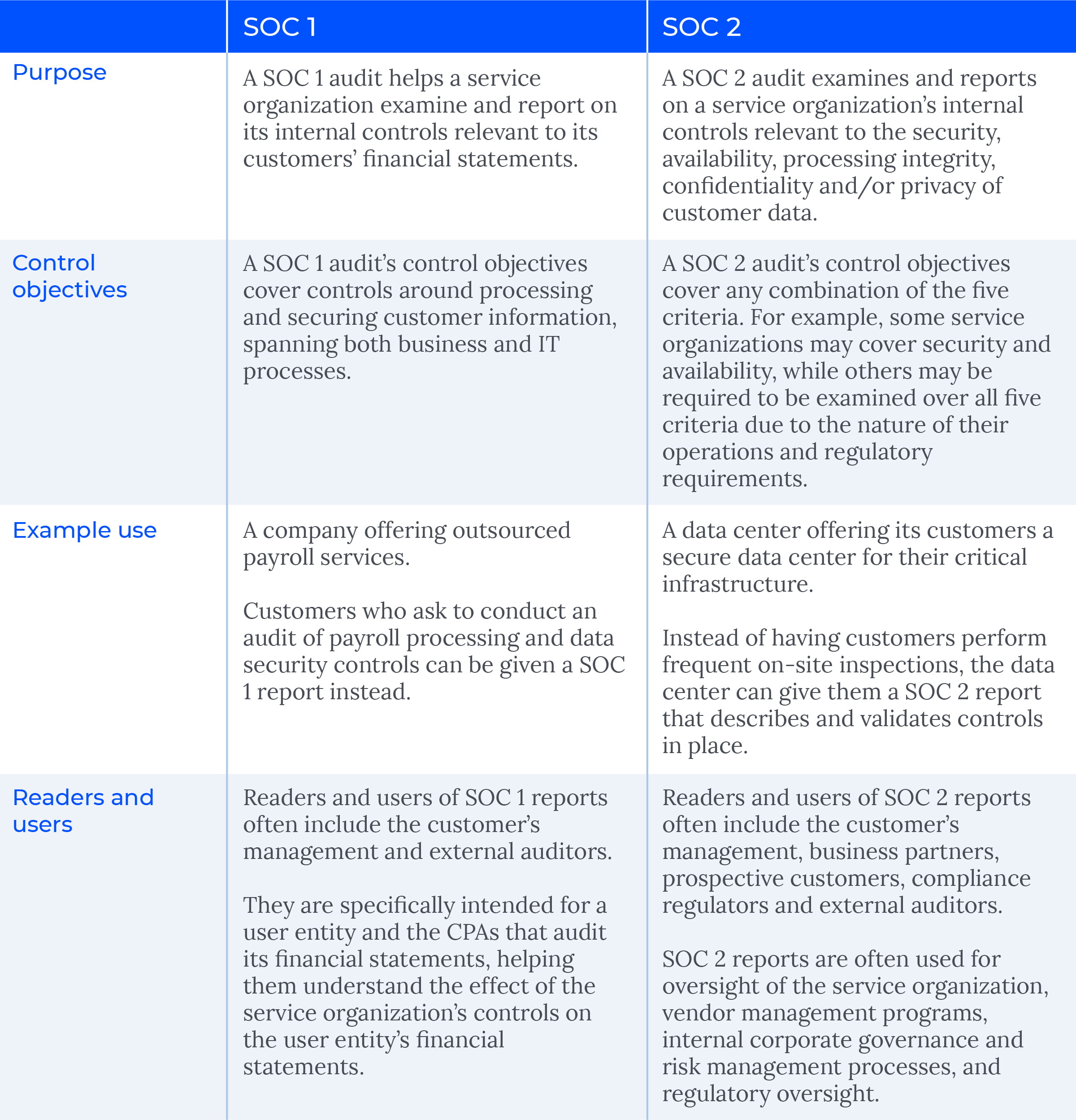

Soc 1 Vs Soc 2 What S The Difference Wipfli

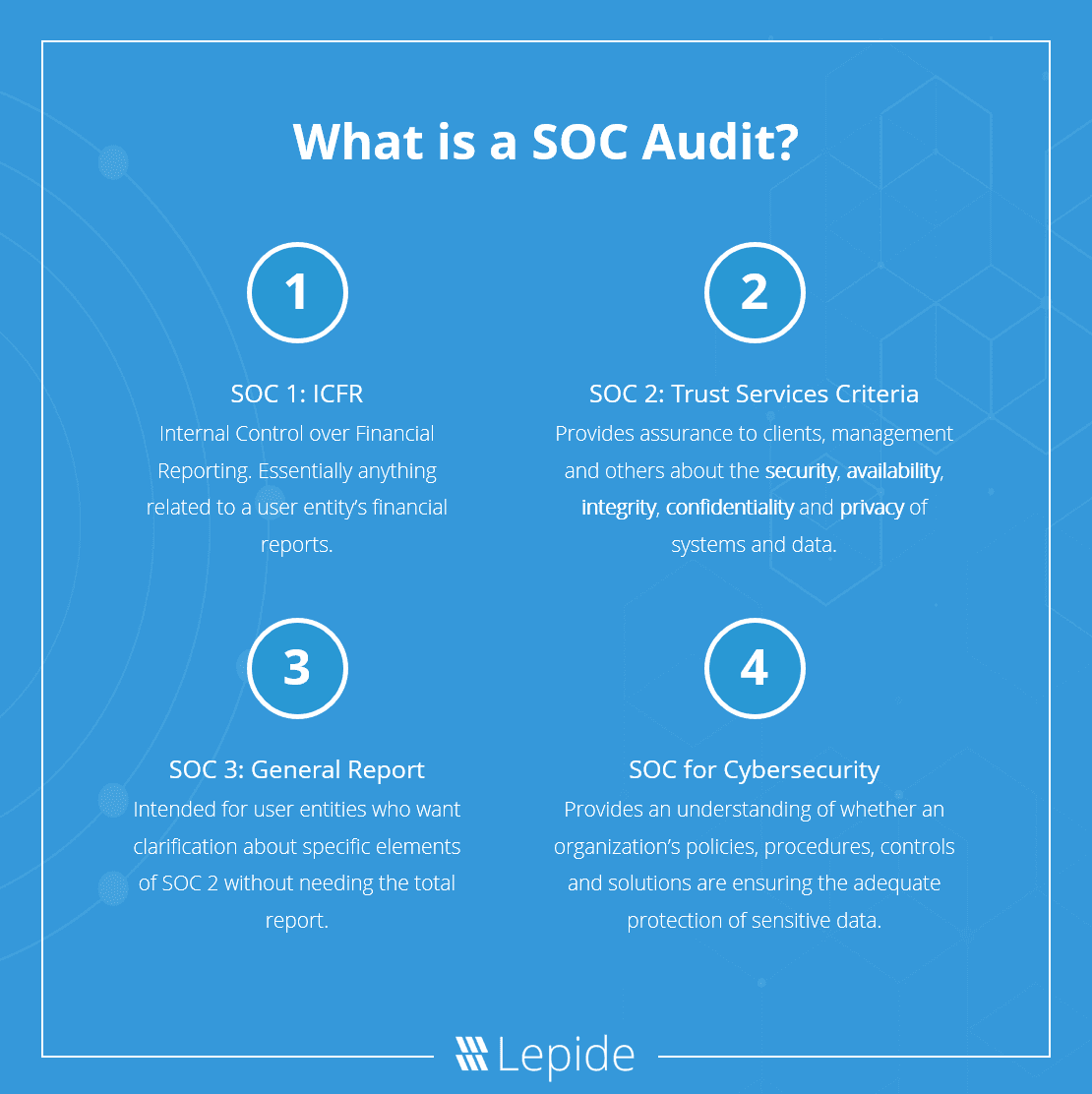

Preparing For A Soc Audit A Checklist

Are necessary to achieve the control objectives stated in management s description of the system when the carve out method of reporting has been used.

Ssae 18 control objectives list.

Ssae 18 Soc Audit And Attestation Services Riskpro India Connect With Risk Professionals

Business Trip Report Template Pdf 3 In 2020 Report Writing Template Sales Report Template Report Writing

Ssae 18 Soc 2 Certified Lifeline Data Centers

Control Objectives Activities What Are They What S Appropriate

Source : pinterest.com